shareholders are still down 74% in the last three years.")

This is definitely a good thing. Guardian Health Inc. (NASDAQ:GH) shares have risen about 58% over the past three months. However, this is only a small consolation in the face of a shocking three-year decline. In fact, the share price has fallen by 74% in the past three years. Therefore, it’s time for shareholders to take advantage. The question to ask is whether the business has truly turned around.

Last week was reassuring for shareholders, but the company is still losing money over the last three years, so let’s take a look at whether the underlying business is causing the decline in performance.

View our latest analysis for Guardant Health

Because Guardant Health made a loss in the last twelve months, the market is probably more focused on revenue and revenue growth, at least for now. When a company isn’t making profits, good revenue growth is usually expected, and as you’d expect, rapid revenue growth often translates into rapid profit growth, if sustained.

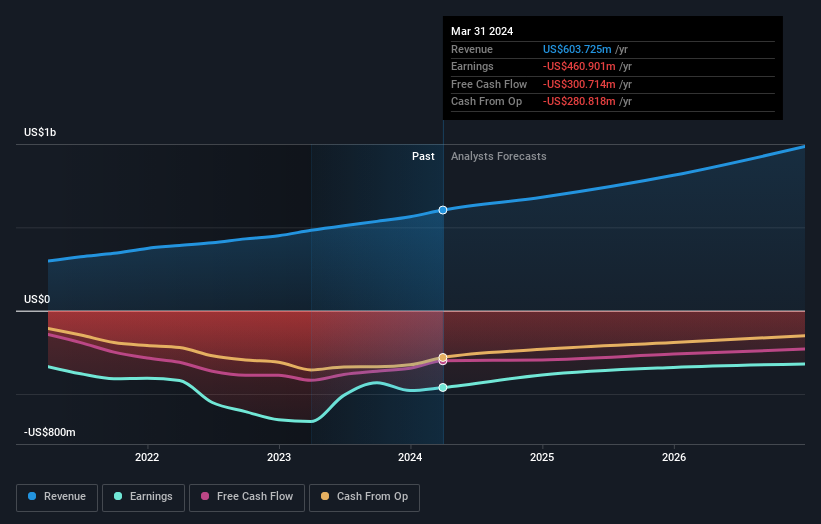

Guardant Health has grown revenues 22% annually over three years, well above most other pre-profitable companies. So why did the stock fall 20% annually over the same period? We need to look at the balance sheet, not just the losses. Rapid revenue growth doesn’t necessarily translate into profits. Without a strong balance sheet, the company may need to raise capital.

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

It’s worth noting that the CEO pay is lower than the average for companies of a similar size. While CEO pay is always worth keeping an eye on, the more important question is whether the company will be able to grow earnings over the next few years. It therefore makes a lot of sense to see what analysts are forecasting Guardant Health’s future earnings (free profit forecasts).

A different perspective

Guardant Health shareholders are down 20% this year, while the market itself is up 23%. Even the share prices of blue chip stocks fall from time to time, but we want to see improvements in the fundamental metrics of the business before getting too interested. Unfortunately, last year’s performance was worse than the 11% annual loss over the past five years, which could indicate unresolved challenges. We know that Baron Rothschild said investors should “buy when the blood is flowing,” but we caution that investors should first make sure they are buying a high-quality business. It’s always interesting to track the long-term movement of a share price. But to better understand Guardant Health, we need to consider many other factors. For example, consider risk. Every company has risks, and we recognize risks. 3 warning signs for Guardant Health You should know.

of course Guardant Health may not be the best stock to buySo you might want to take a look at this free A collection of growing stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

Have feedback about this article? Concerns about the content? contact Please contact us directly. Or email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We use only unbiased methodologies to provide commentary based on historical data and analyst forecasts, and our articles are not intended as financial advice. It is not a recommendation to buy or sell stocks, and does not take into account your objectives, or your financial situation. We seek to provide long-term focused analysis driven by fundamental data. Note that our analysis may not take into account the latest price sensitive company announcements or qualitative material. Simply Wall St has no position in any of the stocks mentioned.